Full Dashboard Screenshot

Every Panel, Explained

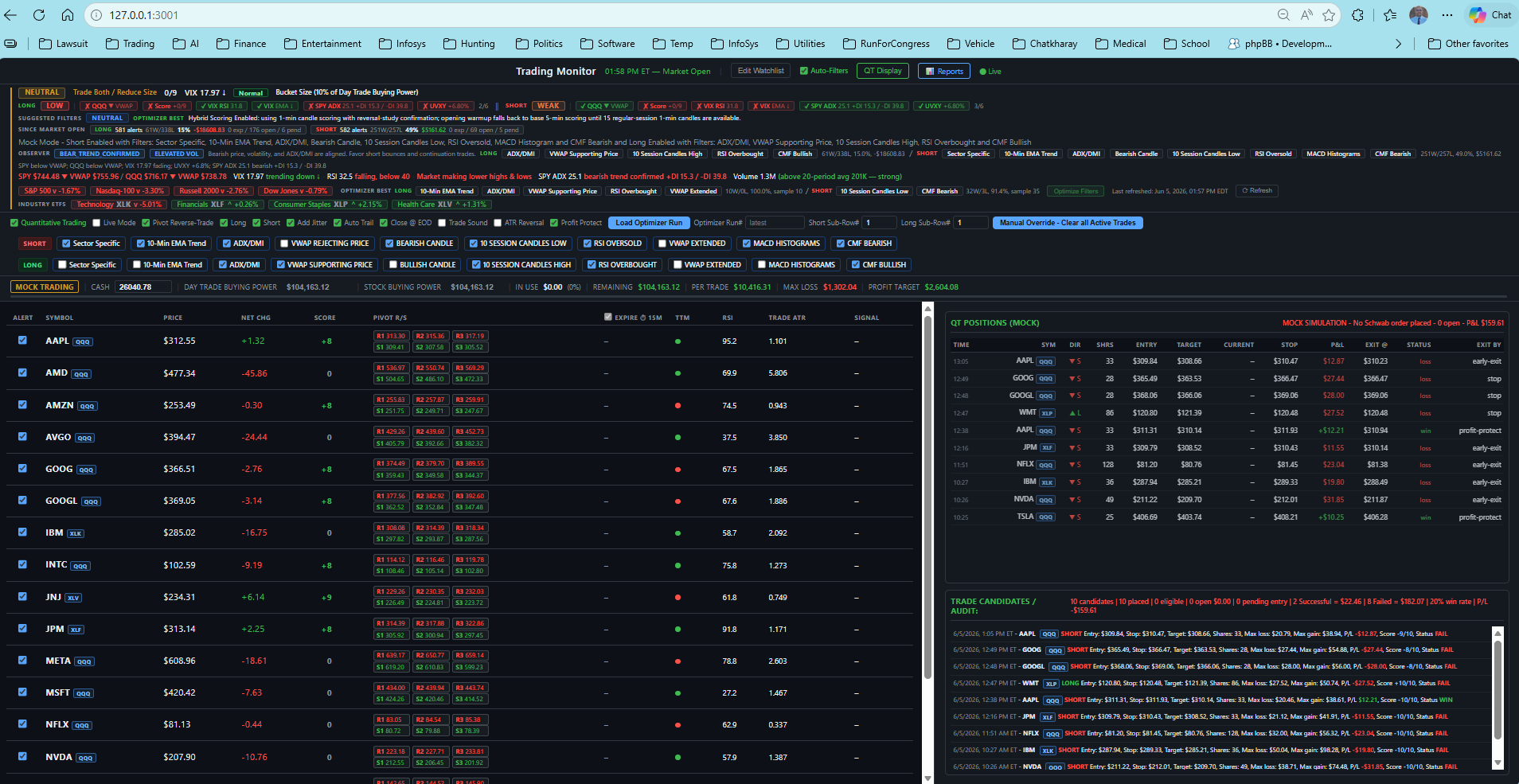

The live interface combines market regime intelligence, watchlist scoring, pivot S/R levels, automated order controls, and real-time position tracking — all in a single view.

1

Market Regime Header

NEUTRAL / BULL / BEAR classification derived from QQQ, VIX, ADX, and SPY scores. Drives Observer Filter Set selection and trade direction gates.

2

Live Alert Counts & Score Summary

Running tally of LONG and SHORT alerts since market open, with the current SPY ADX, VWAP, and VIX readings surfaced inline for quick regime context.

3

Observer Filter Set (OFS) Active Criteria

Auto-Filters applies the optimizer-selected filter combination for the current regime. Shown here: Sector Specific + 10-Min EMA Trend + ADX/DMI + MACD Histograms + CMF Bearish applied to SHORT signals.

4

Industry ETF Momentum Tickers

Live S&P 500, Nasdaq-100, Russell 2000, Dow Jones, and sector ETF (XLF, XLK, XLV) percent-change ribbon. Used for same-sector bias confirmation.

5

QT Automation Controls

The full auto-trade control strip: Quantitative Trading enable, Live Mode (broker orders), Pivot Reverse-Trade, Long/Short direction filter, Add Jitter, Auto Trail, Close @ EOD, ATR Reversal rule, and Profit Protect — all persisted in localStorage.

6

Directional Filter Checkboxes

Per-direction filter toggles: SHORT row (top) and LONG row (bottom). Each filter independently gates signals — Sector Specific, EMA Trend, ADX/DMI, VWAP, Candle Pattern, Session Candles, RSI, MACD, CMF. Optimizer selects the highest win-rate combination.

7

Live Watchlist: Score, Pivot S/R, RSI, TTM, ATR

Each row shows real-time price, net change, confluence score (−10 to +10), three R and three S Pivot levels (daily Standard Pivots), RSI, TTM squeeze state, and Trade ATR used for stop/target sizing. Rows with active signals show the direction badge.

8

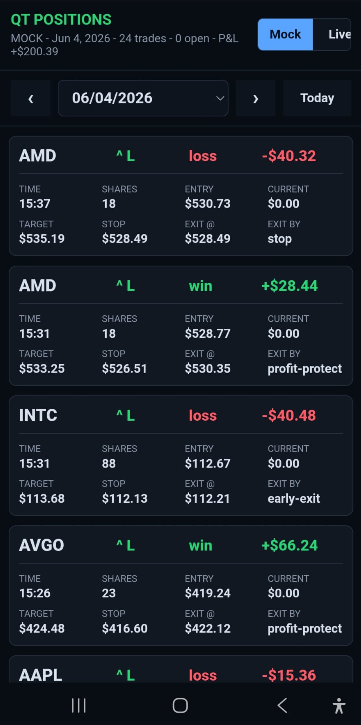

QT Positions Panel (Live / Mock)

Real-time table of all auto-placed trades for the session: entry price, target, current live price, stop, unrealized P&L, exit price, status (open / stop / profit-protect / early-exit). Each row updates every 5 seconds via LEVELONE_EQUITIES quotes.

9

Trade Candidates / Audit Log

Chronological log of every signal that reached the confluence threshold during the session — symbol, direction, entry/stop/target, share count, max loss, max gain, score, and outcome status. Used for end-of-day review and strategy refinement.